We have revised down our near-term house price forecasts but have become more positive over the five-year horizon.

The Middle East conflict has pushed mortgage rates higher, dampened buyer sentiment and fuelled speculation about how the government will respond to the resulting economic shock.

This hat-trick of headwinds means we have revised down our near-term house price forecasts.

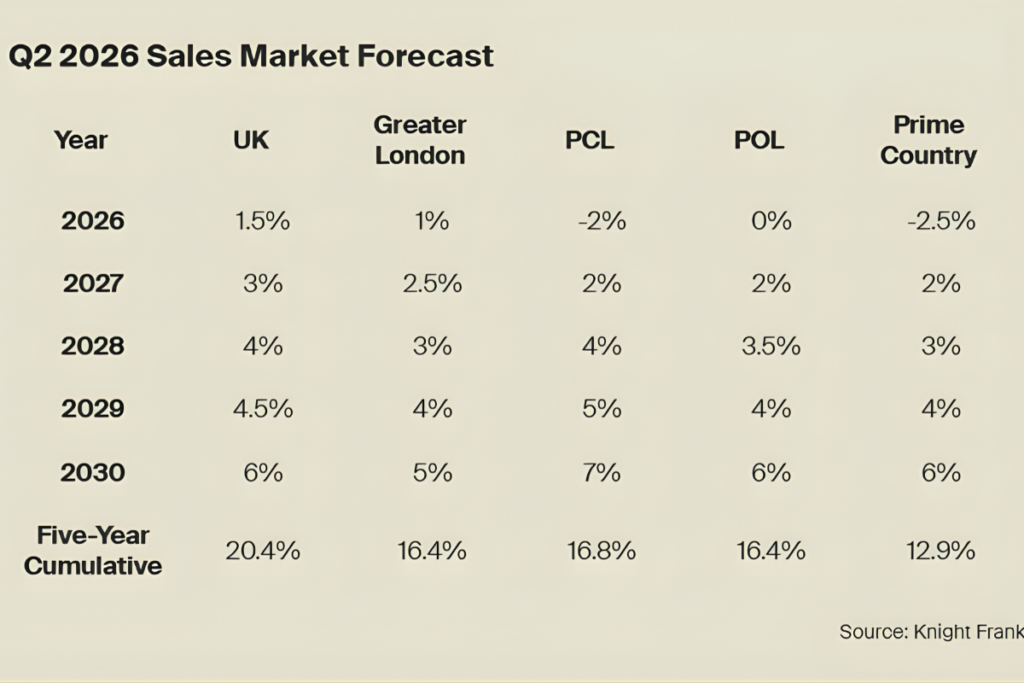

We expect UK house price growth of 1.5% this year, followed by 3% next year and 4% in 2028. That is down from an expectation in September that prices would grow by 3% in 2026 and 4% next year.

UNCLEAR ECONOMIC BACKGROUND

The impact of the Middle East conflict, which began on 28 February, has only just started to influence UK economic data and, for now, the signals remain mixed.

While Halifax reported that UK house price growth fell to 0.8% from 1.2% in March, the Nationwide index increased to 2.1% from 0.9%. Mortgage approval and transaction figures still pre-date the conflict.

Meanwhile, headline inflation started to climb in March thanks to higher energy costs, reaching an expected rate of 3.3%. However, underlying inflation, which strips out food and energy costs, was lower than anticipated at 3.1%, which makes holding rather than hiking rates in April more likely.

Lower unemployment figures this month are also not what they appear. Rather than imply economic strength or build the case for keeping rates high, they reflect a rise in the number of people who have become economically inactive and not counted as unemployed.

INFLATIONARY IMPACT

I discussed the conflict’s longer-term impact on inflation and borrowing costs on a recent episode of Housing Unpacked with Blonde Money CEO Helen Thomas.

In short, we will only know the full impact in coming months, which depends on how long the war lasts and to what extent it escalates.

If it ends relatively soon and UK labour market data stays weak, rate cuts could come back onto the agenda for the Bank of England after an inflation hump of three to six months, according to Michael Brown, an analyst at Pepperstone.

For now, swap rates, which lenders use to price fixed-rate mortgages, have risen notably. The five-year swap rate was trading at around 4% this week compared to just under 3.5% before the war started. However, the figure has come down from 4.3% in March.

It is also worth noting that any effect on house prices will be mitigated by the fact more residential property is owned outright (36%) than with a mortgage (29%) in England.

Another longer-term risk is how the government responds to the economic shock, including the prospect of tax speculation ahead of the autumn Budget. This year, there is the added uncertainty of whether Rachel Reeves and Keir Starmer will be in Downing Street after the summer.

Making predictions at the moment comes with a particularly long list of caveats.

PRIME MARKETS

We also expect higher rates to have an impact in prime markets, despite the fact buyers and sellers are typically more discretionary and hold more equity.

Prices in prime central London are forecast to drop by 2% this year, as opposed to an expectation in September they would be flat. Similarly, we think prices in prime outer London will be flat in 2026, which is down from our previous forecast of 2%.

Furthermore, we expect average prices in the prime Country market, an area that covers a range of £750,000-plus rural and urban locations outside London, to fall by 2.5% in 2026. They declined by 5.5% in the year to March.

While prime markets will be less affected by the jump in borrowing costs itself, we expect geopolitical uncertainty and speculation around further tax rises will keep demand in check.

As a result of the threat from the Green Party, I discussed how the Labour government is likely to move to the political left, irrespective of who is in charge, on a recent episode of Housing Unpacked with James Nation, a former deputy head of the Number 10 Policy Unit.

There is an obvious contrast with 2009, when geopolitical instability drove overseas capital into prime central London following the Global Financial Crisis.

Although there have been some cases of people moving to London from the Middle East since February, the increase in demand has been more notable so far in the rental market.

LONGER TERM UPLIFT

We have raised our longer-term forecasts on the assumption that a new government will take office in 2029.

Given how UK politics has fragmented since the general election in July 2024, the composition and durability of any new government is uncertain.

However, current polling suggests policy will be shaped by a stronger instinct for lower taxes and a tighter control over government spending.

Such an approach has the potential to put downwards pressure on government borrowing costs and improve affordability in the housing market. Meanwhile, any wealth-related incentives would underpin demand in prime markets.

The Conservative Party, for example, has said it will scrap stamp duty to stimulate economic growth. It would not be a straightforward process but, as we have seen in recent years, a party does not need to be in power to shift thinking on policy, especially if it resonates with the electorate.

A wider question politicians will certainly need to address is whether taxing property transactions makes fiscal sense.

While the composition of the next government is highly uncertain, we believe a change in political direction will underpin annual house price growth of more than 5% in mainstream and prime markets in 2030.

RENTAL MARKETS

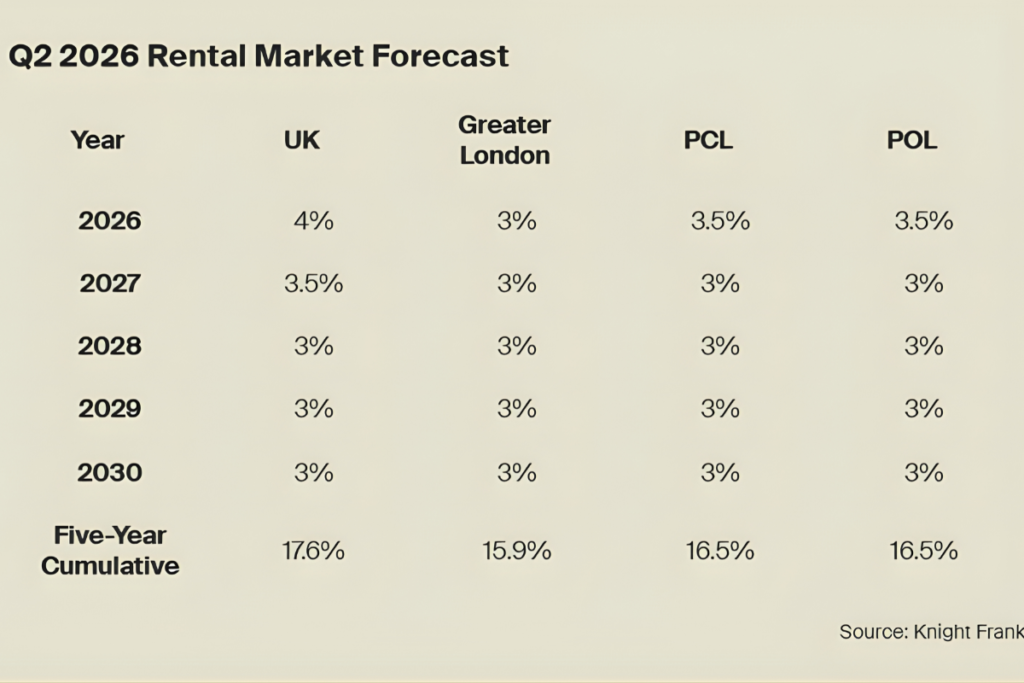

We have lowered our rental forecasts marginally, but upwards pressure on rents will persist this year following the introduction of the Renters’ Rights Act.

The new rules, which come into effect on 1 May, raise the risks for landlords around repossessing or selling their property, setting rents and guaranteeing rental income. These additional risks will require extra reward and put upwards pressure on rents.

This may be exacerbated by tighter supply as more landlords leave the sector once the new rules are in force. We expect 3.5% annual growth in prime central and outer London this year, up from the current respective rates of 1.2% and 2.8%.

Rental activity will also benefit in the short-term as demand moves across from the sales market as higher borrowing costs curb spending power and the current geopolitical uncertainty means people keep their options open.

Activity has also been supported to some extent by people looking to temporarily move back to London from the Middle East.

Tighter rules around energy efficiency standards will also deter some landlords in the longer-term and put upwards pressure on rents, as discussed on a recent episode of Housing Unpacked with Louisa Sedgwick, head of mortgages at buy-to-let specialist Paragon Bank. Landlords will need to ensure their properties have an EPC C rating by 2030.

“This particular change in legislation I think is going to be bigger and potentially more demanding (than the Renters’ Rights Act) because I don’t believe we’ve got the infrastructure to support it,” said Sedgwick.