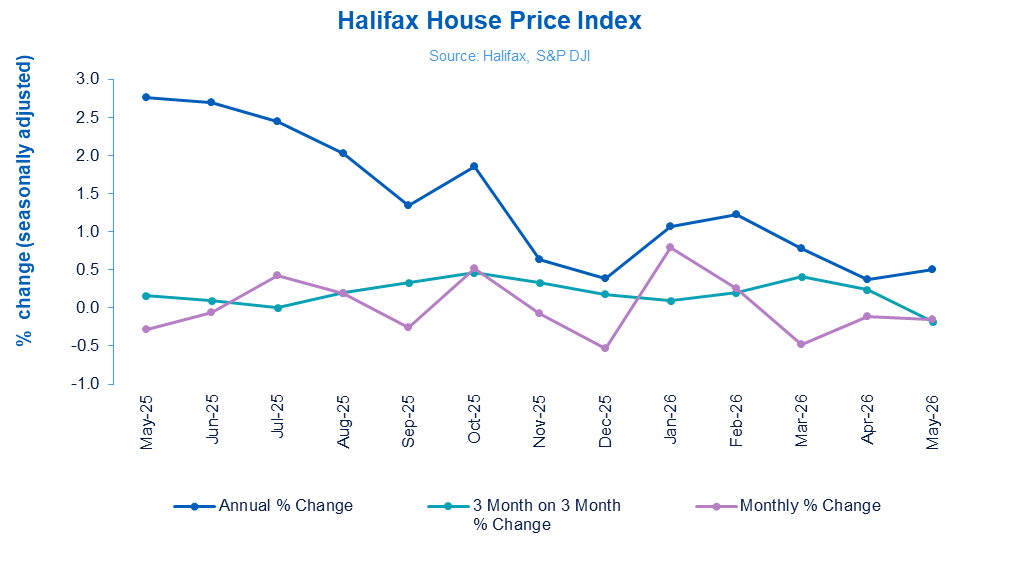

UK house prices remained largely unchanged in May with Halifax reporting on Friday last week a second consecutive monthly fall of just -0.1% as the market continued to demonstrate resilience despite global economic uncertainty.

The latest Halifax House Price Index shows the average UK property now costs £298,806, compared to £299,251 in April. Annual house price growth edged up slightly to 0.5%, from 0.4% the previous month.

While the headline figures point to a relatively stable market, regional variations remain pronounced, with northern regions and the devolved nations continuing to outperform much of southern England.

Northern Ireland once again recorded the strongest annual growth across the UK, with prices rising by 7.8% to an average of £227,177. Scotland also posted robust growth of 3.8%, taking the average property value to £222,650.

BROADLY STABLE

Within England, the North East led the way with annual growth of 3.1%, while the North West saw prices rise by 3.0% over the year.

In contrast, house prices continued to soften across parts of southern England. The South East recorded the largest annual decline, with values falling 2.1% to £382,704, while London prices were down 1.5% year-on-year, leaving the average property value at £534,375.

Amanda Bryden (main picture, inset), Head of Mortgages at Halifax, says: “Average house prices remained broadly stable in May, with a slight fall of -0.1% matching that seen in April. The typical property now costs £298,806, while the pace of annual growth edged up slightly to +0.5%.

“Property price trends continue to reflect the uncertainty linked to developments in the Middle East.

“Despite recent cuts to mortgage rates, higher inflation expectations have kept borrowing costs above the level seen at the start of the year, continuing to stretch affordability for many buyers and temper demand.

“Even so, overall activity has held up well, reflecting the underlying resilience of the UK housing market. Latest industry figures show transaction levels remain relatively stable, suggesting buyers and sellers are still moving.”

FIRST-TIME BUYERS

Halifax also pointed out that that first-time buyer house price growth remains subdued at 0.3%, reflecting the affordability pressures still facing those looking to enter the market.

However, lenders have continued to introduce more flexible affordability assessments and a wider range of low-deposit products to support buyers.

Looking ahead, Bryden believes borrowing costs and consumer confidence will remain the key drivers of activity.

She adds: “Looking ahead, borrowing costs and consumer confidence are likely to continue shaping activity in the coming months, with house prices expected to be broadly stable while interest rates stay elevated.

“The housing market remains closely tied to wider global developments, with a return to sustained house price growth dependent on an improvement in the inflation outlook and a fall in mortgage costs.”

INDUSTRY REACTION

Nathan Emerson, CEO of Propertymark, says: “A dip in house prices both month on month and quarterly highlights the ongoing impact of affordability pressures on buyer behaviour, particularly as many households continue adjusting to higher mortgage repayments and wider cost-of-living concerns.

“Although demand has moderated, the market remains active, where sellers are willing to align pricing with local conditions.

“Buyers are becoming more selective, and professional guidance is increasingly important in helping transactions progress smoothly.”

POLITICAL UNCERTAINTY

Tom Bill, Head of UK Residential Research at Knight Frank, says: “The seasonal spring bounce in the property market has fallen flat this year.

“Prices and transaction volumes have been squeezed by higher mortgage rates due to the Middle East conflict and the inflation signals suggest that borrowing costs won’t drop meaningfully in the short term.

“Uncertainty around the political direction of the government and whether any future Chancellor could raise taxes further may also keep demand in check, which means we expect minimal UK house price growth of 1.5% this year.”

PRAGMATIC OUTLOOOK

Jason Tebb, President of OnTheMarket, says: “Despite political uncertainty and challenging economic conditions, needs-driven buyers and sellers who may have delayed making moving decisions last year are focused on transacting.

“While affordability concerns remain, easing mortgage rates are helping focus minds, with borrowers adapting to shifting market conditions and securing cheaper rates while they are available.

“Little movement in average house prices suggests buyers and sellers are adopting a pragmatic outlook and adjusting expectations, rather than a loss of confidence.

“Steadier prices are better as far as those trying to get on the ladder for the first time are concerned, as there is less risk of being priced out further, although Halifax notes that their numbers are a little subdued.

“This is the strongest buyers’ market we have seen in many years, with plenty of stock to choose from.”

COOLING NOT COLD

Verona Frankish, CEO of Yopa, says: “A cooling market isn’t the same as a cold market.

“Whilst house prices have remained largely flat in recent months, the fact that mortgage approvals have climbed to their highest level in more than a year tells us that buyers are still very much engaged.

“Stability may not grab the headlines, but it’s exactly what the market needs after a prolonged period of volatility.”

BUDGETS AND EXPECTATIONS

Chris Hodgkinson, Managing Director of House Buyer Bureau, says: “The biggest gap in today’s market isn’t between supply and demand, it’s between buyer budgets and seller expectations.

“Buyers are continuing to move, but they’re negotiating harder than they have for years and they’re unwilling to overpay.

“Sellers who remain anchored to yesterday’s market values risk spending longer on the market and accepting a lower offer further down the line.”

NOT A SPRINT

Marc von Grundherr, Director of Benham and Reeves, says: “The housing market has become a marathon rather than a sprint, but buyers are still crossing the finish line.

“Whilst we’re not seeing the consistently strong monthly rates of growth seen in previous years, house prices continue to strengthen on an annual basis and market activity remains remarkably resilient.”

MARKET MISMATCH

Amy Reynolds, Head of Sales at Richmond estate agency Antony Roberts, says: “The market is defined by a mismatch: cautiously-motivated sellers, cost-conscious buyers with genuine negotiating power, and a conveyancing system struggling to get deals over the line – a serious problem when mortgage rates can spike almost overnight.

“With the Bank of England meeting in a fortnight to review interest rates, an increase could shatter the cautious optimism we’ve seen over the past few weeks. This market needs stability and it needs transactions – and frankly, so does the country.

“Stamp duty is a significant contributor to Treasury revenues, and with transaction numbers already under pressure, the tax take is falling.

“A cut in stamp duty would stimulate activity, protect jobs in the property supply chain and raise taxes. I suspect instead stamp duty will stay as it is but the housing market is fragile and needs supporting.”

REMARKABLY RESILIENT

Iain McKenzie, CEO of The Guild of Property Professionals, says: “The latest Halifax figures reinforce the picture of a housing market that is proving remarkably resilient despite a challenging economic backdrop.

“While prices dipped marginally by 0.1% in May, annual growth has edged higher and values remain broadly stable, demonstrating that underlying demand continues to support the market.

“Buyers are navigating a complex environment, with geopolitical tensions, inflationary pressures and higher borrowing costs all weighing on confidence.

“However, committed movers are still transacting, reflected in sales agreed running ahead of last year and mortgage approvals remaining close to long-term averages.

“There are reasons for cautious optimism. Inflation has eased from recent highs, and although expectations of future rate cuts have become less certain, lenders have continued to reduce mortgage rates in recent weeks as competition for business intensifies. This is providing welcome support for affordability and helping buyers who have been waiting on the sidelines.

“The market appears well balanced rather than booming or declining.”

“At the same time, an increase in the number of homes coming to market is creating greater choice for purchasers and helping sustain activity levels. That said, buyer demand remains softer than a year ago and many households are still carefully assessing their finances, meaning realistic pricing will remain critical for sellers.

“Looking ahead, the market appears well balanced rather than booming or declining. Transaction levels are holding up in line with seasonal expectations, but ongoing uncertainty surrounding inflation, interest rates and wider global events means the housing market is likely to continue its steady, measured path through the remainder of 2026.”

PRICE WOBBLE

Jeremy Leaf, north London estate agent and a former RICS Residential Chairman, says: “Viewings, listings and even agreed sales may be holding up relatively well but the difficulty in obtaining commitment due principally to worries over the Iran conflict impacting the cost of living, is starting to make itself felt.

“Most buyers are taking their time to try to ensure as far as possible they have found the right place and are not overpaying.

“As a result, prices are wobbling a bit and transactions are taking longer to complete, which is increasing fall throughs. We are finding though that some stability will certainly increase confidence in the medium to longer term.”

LENDER SOLUTIONS

Mark Harris, Chief Executive of mortgage broker SPF Private Clients, says: “As Swap rates, which underpin the pricing of fixed-rate mortgages, continue to fall, so lenders continue to trim their mortgage rates, which is helping ease affordability.

“However, the steadiness in house prices suggests buyers are still prepared to negotiate hard and are not willing to pay over the odds.

“First-time buyers will be encouraged as house prices remain steady rather than soar.

“Lenders are working hard on offering solutions to those trying to get on the ladder for the first time, which is leading to a small improvement in their numbers.”

UNCERTAIN CLIMATE

Tomer Aboody, director of specialist lender MT Finance, says: “With rates and inflation still unsettled and on the higher side, buyers are trying to stay active.

“More activity in the market is being encouraged as more sellers are coming to the market, and buyers finally having some stock to look at.

“With the macro climate still uncertain and rates potentially going to be higher by the end of the year, buyers are not wanting to hang around and wait.”

GRIM PICTURE

Jeremy Matallah, Co-founder of Keyzy, says: “House prices are tumbling in real terms. Normally that spells relief but rents are too high, home building is still scarce and income multiples are brutal. This isn’t a market correcting, it’s a market freezing over.

“It’s a grim picture. We’ve built a housing market that can’t do the two things we most need it to, which is create new homes that people can afford.

“It’s no good just pinning the blame on build costs, that’s ducking the real issues. Stamp duty also has a lot to answer for, as do monthly mortgage repayments which are hammering budgets in a way that just didn’t happen a decade ago when rates were on the floor.

“For vendors, the picture is bleak and motivated sellers need to get real on price. They’re going to have to become even more realistic about valuations, while buyers upsizing or buying for the first time have no reason to rush.

“They’ve got every incentive to wait to see if mortgage rates come down alongside further price falls. It’s a classic doom loop for vendors, and first-time buyers may yet be this year’s real winners.”