House prices remained broadly flat in April as higher mortgage costs and renewed economic uncertainty continued to weigh on buyer confidence according to the latest Halifax House Price Index.

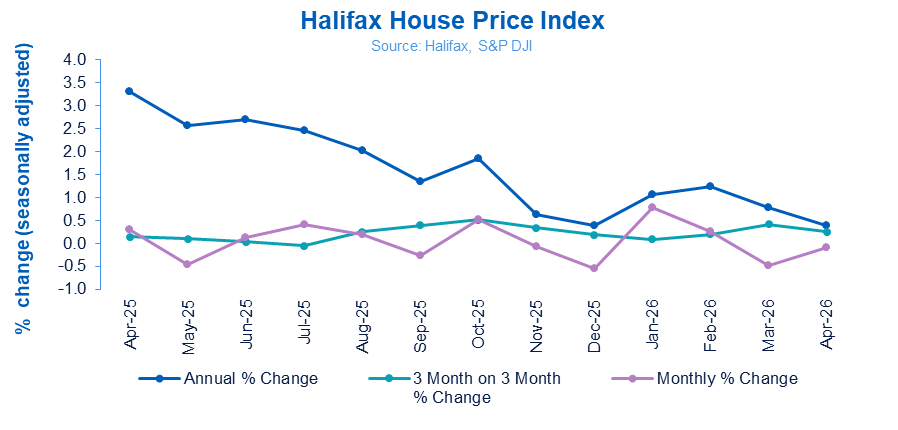

The lender said average UK property prices dipped by -0.1% during the month, following a -0.5% decline in March, leaving the average home valued at £299,313.

Annual house price growth also slowed to +0.4%, down from +0.8% the previous month, as affordability pressures and rising borrowing costs tempered market activity.

The latest figures suggest the housing market is entering a more cautious phase after a relatively resilient start to 2026, with buyers increasingly sensitive to mortgage pricing and wider cost-of-living pressures.

ECONOMIC UNCERTAINTY

Amanda Bryden (main picture, inset), Head of Mortgages at Halifax, says: “Average house prices showed little movement in April, edging down by just -0.1% compared to March, with the typical property now costing £299,313. The pace of annual growth also eased to +0.4%.”

She says recent global developments and higher energy prices have increased uncertainty around inflation and interest rates, adding that markets had “reassessed the path for interest rates”, which had already pushed up borrowing costs for many buyers.

Bryden adds that while activity could cool in the near term, the housing market continued to show resilience, supported by wage growth continuing to outpace house price inflation.

AFFORDABILITY PRESSURES

The data also points to growing affordability pressures for first-time buyers, although Halifax said more stable pricing could provide some support for those trying to get onto the property ladder.

The lender said the average price paid by a first-time buyer fell slightly to £238,908, its lowest level so far this year.

Regional performance continued to show a strong North-South divide.

Northern Ireland recorded the strongest annual growth at +7.6%, with average prices reaching £224,851, while Scotland posted annual growth of +4.0% to £222,448.

In England, the North East saw prices rise +4.5% annually, while the North West recorded growth of +3.4%.

By contrast, southern markets remained weaker. The South East recorded the largest annual fall at -2.0%, while London prices declined -1.4% year-on-year to £536,051.

INDUSTRY REACTION

Nathan Emerson, CEO of Propertymark, says: “Despite ongoing uncertainty within the economy, it is reassuring to see a position of consistency concerning house prices currently.

“However, it is imperative to note that many people may face future affordability challenges until there is sustained de-escalation concerning current global unrest.

“The rate of inflation remains a key concern for many people, especially as there is widespread speculation that the Bank of England may potentially need to implement measured base rate increases over the coming months to best regulate potential future financial instability.

“There will likely be a sense of anxiety across the summer months, especially for those with tracker mortgage products, and with mortgage deals that are due to expire.

“It will be important for people to investigate what new mortgage products might be available to them and to make plans to help navigate around any increased expenditures.”

REDUCED SPENDING POWER

Tom Bill, head of UK residential research at Knight Frank, says: “The recent spike in mortgage rates will only put gradual downwards pressure on house prices as more favourable offers that pre-date the Middle East conflict take several months to lapse.

“It means some buyers are keen to complete while others have seen their spending power reduced.

“We expect house prices to begin falling in coming months but modest growth to return by the end of the year.

“However, that will depend on how long the conflict lasts, to what extent it escalates and how the government responds to the economic shock, whoever is Chancellor at the time of the next Budget.”

STABILITY A POSITIVE SIGN

Iain McKenzine, CEO of The Guild of Property Professionals, says: “While Halifax’s latest figures show that house prices remained broadly flat in April, this really underlines the resilience of the UK housing market against a backdrop of continued economic and geopolitical uncertainty.

“A marginal monthly dip of -0.1% and annual growth of +0.4% points to stability rather than any significant correction in values.

“Higher inflation and the Bank of England’s decision to hold interest rates at 3.75% have naturally influenced sentiment, particularly as mortgage pricing reacted to wider global events.

“However, in recent weeks we seen mortgage rates becoming more competitive, as lenders sharpen their pencils to stimulate activity and support buyer demand.

“There are some more positive signs emerging.”

“Encouragingly, there are some more positive signs emerging. GDP growth has returned, mortgage approvals are improving, and transaction volumes reached their highest seasonally adjusted level since March last year.

“While buyer demand remains below 2025 levels, the trend has been relatively consistent throughout the year, suggesting the market is steady rather than deteriorating.

“Importantly, agreed sales are only marginally below last year’s levels, showing that committed buyers and sellers are continuing to move despite wider economic headwinds.

“Needs-based movers remain active and continue to drive transactions, while more discretionary movers are understandably taking a little longer to assess the market and wider economic outlook before making decisions.

“Overall, the housing market continues to demonstrate resilience. Activity may not be booming, but stability in the current climate should be viewed as a positive sign for the sector.”

BUYER REASSURANCE

Guy Gittins, CEO of Foxtons, says: “A very marginal monthly dip in house prices is unlikely to cause concern and reflects the more measured pace of the market seen so far this year, particularly against the heightened turbulence of the wider economic backdrop.

“At Foxtons, demand was up in April and we’re confident the recent decision to hold the base rate will provide further reassurance to buyers about the overall resilience of the UK property market.”

HOLDING FIRM

Verona Frankish, CEO of Yopa, says: “A small monthly adjustment is nothing to be concerned about and the underlying strength of the market remains very evident when you look at the broader trend.

“House prices are continuing to hold firm despite ongoing affordability pressures and that’s a clear sign that buyer appetite remains strong, particularly amongst those who have adapted to higher borrowing costs and are now keen to press on with their move.”

GROWING DISCONNECT

Chris Hodgkinson, Managing Director of House Buyer Bureau, says: “The problem facing the market at the moment is that many sellers are still pricing based on expectation rather than current market reality and that’s creating a growing disconnect between buyers and sellers.

“Whilst demand is still there, buyers are far more price sensitive in the current climate and homes that aren’t positioned correctly from day one are simply sitting on the market for longer, forcing sellers into larger reductions further down the line.”

STABILITY AND RESILIENCE

Marc von Grundherr, Director of Benham and Reeves, says: “While the market may have paused for breath on a monthly basis, the wider picture remains one of stability and resilience and that’s particularly encouraging given the economic uncertainty seen so far this year.

“Buyer demand across London has remained consistent and, with mortgage rates continuing to improve, we expect confidence to strengthen further as we move through the summer market.”

STEADY ACTIVITY

James Nightingall of property search service HomeFinder AI, says: “In April, some house hunters took a break to enjoy the Easter holidays whilst others ceased the opportunity to arrange viewings or put in an offer.

“Although buyer interest remains steady overall, the property market hasn’t seen the spike in activity usually associated with Spring as interest rates and geopolitical developments continue to fuel uncertainty.”

AFFORDABILITY CONCERNS

Jason Tebb, President of OnTheMarket, says: “Despite challenging economic conditions and political uncertainty, needs-driven buyers and sellers who may have put moves on hold last year are showing resilience and remain focused on transacting.

“While affordability concerns remain, rather than retreating from the market, borrowers are adapting and grabbing lower mortgage rates while they can.

“Little movement in average house prices suggests buyers and sellers are adopting a pragmatic outlook and adjusting expectations, rather than a loss of confidence. A market that is not running away with itself is also encouraging for first-time buyers who are vital to enable transactions to take place further up the ladder.

“Our own property sentiment index shows that the market is adapting to change, treating volatility as part of the landscape rather than a reason to delay decisions.”

A NEW NORMAL

Jeremy Leaf, north London estate agent and a former RICS Residential Chairman, says: “These historically-reliable figures confirm much of what we are seeing in our offices – housing market activity may not be what it was just a few months ago, when it was growing steadily, but buyers and sellers are coming to terms with a ‘new normal’ of uncertainty with regard to mortgage rates and inflation.

“We are finding it is harder to gain commitment with so much choice of property as buyers negotiate hard and try to convince themselves that they are still getting value for money.”

NOT SPECTACULAR

Amy Reynolds, head of sales at Richmond estate agency Antony Roberts, says: “The market feels steady rather than spectacular with buyers still active but more selective, more analytical on pricing and far more aware of monthly mortgage costs than they were a year ago.

“That said, we are finding that demand for quality family houses in the Richmond Borough remains robust because supply continues to be relatively limited. We are seeing realistic sellers being rewarded with good levels of viewings and competitive offers, while overpriced properties are sitting on the market for much longer.

“While the London market saw average values fall according to Halifax’s data, there is little evidence locally of any significant correction in prime family house values, more a correction on inflated asking prices.”