Price expectations have improved in needs-driven markets, but political uncertainty means we have cut the near-term growth outlook for prime central London.

The interest rate environment is improving and not just because the Bank of England cut by 0.25% to 4.25% last week.

The more important consideration is that markets are pricing in between two and three further cuts this year, which means fixed-rate mortgages are getting cheaper. It should underpin demand in the UK housing market this spring irrespective of whether the cuts happen, or inflation eventually puts upwards pressure on borrowing costs again.

Six months ago, financial markets were pricing in the equivalent of less than one cut between now and December. Easing inflation concerns, weaker economic data and tariff turbulence have improved the chances of lower rates.

MIXED SIGNALS

Alongside the cut, there were mixed signals from the Bank of England, which said rates were not on a “preset path”. In wording that was slightly more hawkish than anticipated, it was a reference to the tariff-induced uncertainty.

For anyone looking for a more positive spin, they could highlight how two members of the nine-strong monetary policy committee voted for a 0.50% cut or how the Bank now thinks inflation will peak at 3.5% rather than 3.7% in Q3 this year.

The economic headlines have also been dominated by the outline trade deal agreed between the US and the UK that will reduce tariffs for certain industries. The more hawkish-than-expected tone from the Bank of England and the improved economic outlook following the deal announcement meant UK borrowing costs rose slightly in trading on Friday.

The changed rate environment means it is an appropriate time to revisit our UK house price and rental forecasts. They were last revised in November in the wake of a Budget that was considered inflationary and left the government with less financial headroom than bond markets would have liked.

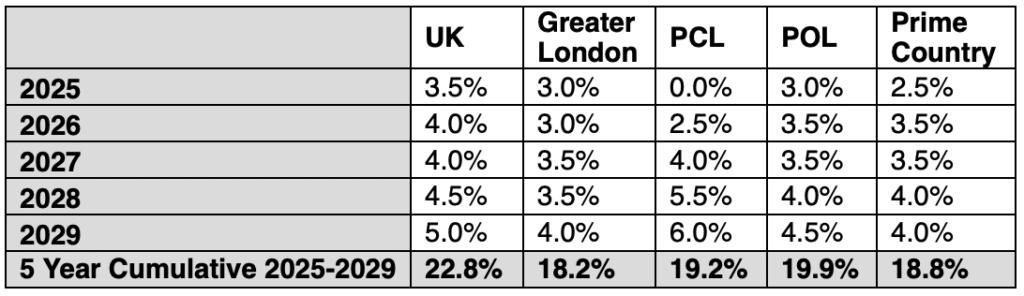

THE SALES MARKET

We have revised up our estimate for UK prices to 3.5% from 2.5% this year due to the improving rate landscape. The figures have also risen slightly over the following three years, taking the cumulative five-year total to 22.8% from 19.3%.

For the same reasons, we have pushed our forecast for Greater London slightly higher, with five-year growth increasing to 18.2% from 15.3%.

We think the more favourable rate environment will also underpin demand and prices in the needs-driven markets of prime outer London and the prime country market, which covers a range of rural and urban markets above £750,000 outside the capital.

However, we have cut our near-term forecast for prime central London due to the fact the political backdrop has become more uncertain for higher-value markets over the last six months.

“We now think prices will be flat in 2025 rather than rise by 2%.”

We now think prices will be flat in 2025 rather than rise by 2% but the relatively small drop in cumulative growth expectations (19.2% now versus 21.6% in November) underlines how strong price growth could quickly materialise in a market where average prices are down by 18% over the last decade.

The government showed little flexibility in its negotiations with groups representing wealthy overseas investors and decided to scrap the UK’s non dom regime in favour of a new scheme that makes the country less competitive on the international stage.

It means a number of non doms have left the UK and demand in prime markets remains subdued. While average prices in PCL fell 1.6% in the year to April, they rose 1.2% in prime outer London.

Despite the uncertainty, the recent tariff turbulence means the UK could ultimately capitalise on its image as a stable place to invest by default.

Furthermore, the recent local election results suggest internal disquiet may grow about the direction the government is taking.

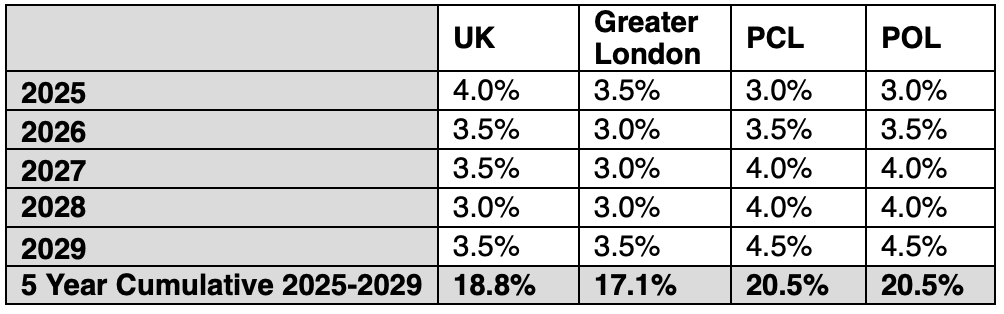

THE RENTAL MARKET

Our rental forecasts are largely unchanged, but we have revised up our expectations for the UK and Greater London marginally due to the ongoing supply squeeze.

We expect cumulative growth of 18.8% in the UK (17.6% in November) and 17.1% in London, up from 15.3% six months ago.

The expected introduction of the Renters’ Rights Bill later this year is one factor driving supply lower and rents higher.

The new rules will make it harder for landlords to reclaim possession of their property and increase the risks around the collection of rent.

The number of new rental listings in England in the first quarter of this year is still 18% lower than it was in the same period in 2019, Rightmove data shows.

“The prospect of tougher green regulations and rising mortgage costs are also squeezing supply as some landlords opt to sell.”

The prospect of tougher green regulations and rising mortgage costs are also squeezing supply as some landlords opt to sell.

For example, private rented homes will need a minimum Energy Performance Certificate rating of C from 2030. The tougher requirement is why we have revised up our forecasts marginally across all areas in 2029.

We expect rental demand to be resilient over the next five years, due to affordability pressures in the sales market which will only intensify as mortgage rates normalise from the low base of recent years.