The UK’s housing market has long been characterised by the simple and depressing narrative that homeownership is out of reach for younger generations.

The statistics seem to confirm this pessimism with one third of aspiring buyers believing they will never own their own home.

However, latest research from the Building Societies Association reveals an unexpected barrier as nearly half of would be first time buyers have never even checked what mortgage options are available to them.

This is an information failure that’s keeping thousands of people trapped in expensive rental markets when they could be homeowners.

THE FIRST-TIME BUER PERCEPTION GAP

The data paints a picture of disconnection between the desire to own a home and the belief that it’s achievable. According to the BSA’s research of 1,000 prospective first-time buyers, 47% have never spoken to a lender or mortgage broker to explore their options.

Even among those who have, 46% haven’t done so in the past year which means they will have been unable to pick up on the latest product innovations or rate changes.

When shown what building societies actually offer, including low and no deposit mortgages, 67% of respondents said they could buy a home sooner than they thought. It seems people are ruling themselves out of home ownership before they even understand what’s possible.

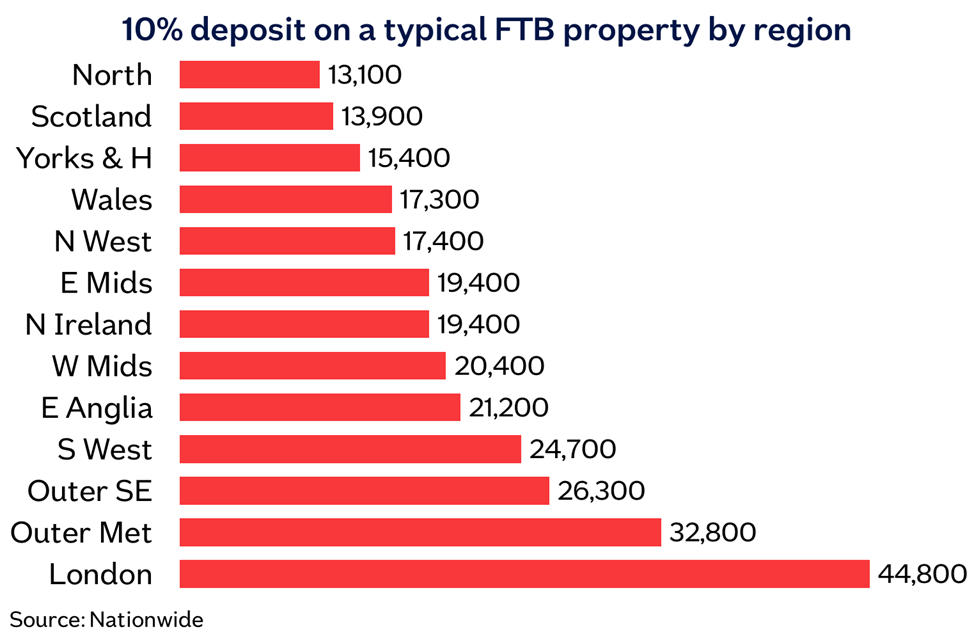

The deposit hurdle looms large in the public imagination. Nationwide’s House Price Index data shows that a 10% deposit on a typical first-time buyer property now sits at around £23,000.

For someone saving 10% of average net pay (approximately £320 per month), that deposit would take nearly six years to accumulate. The psychological weight of that timeline inevitably puts some people off.

Building societies provided 35% of all first-time buyer lending in 2025, with 23% of that going to borrowers with deposits below 5%. Nearly half (46%) of building society first-time buyer mortgages went to people under 30 and 10% to buyers over 45, demonstrating that the sector is actively serving demographics that other lenders might overlook.

THE EMERGING AFFORDABILITY IMPROVEMENT

While the national conversation remains stuck on affordability, something important has been happening beneath the surface.

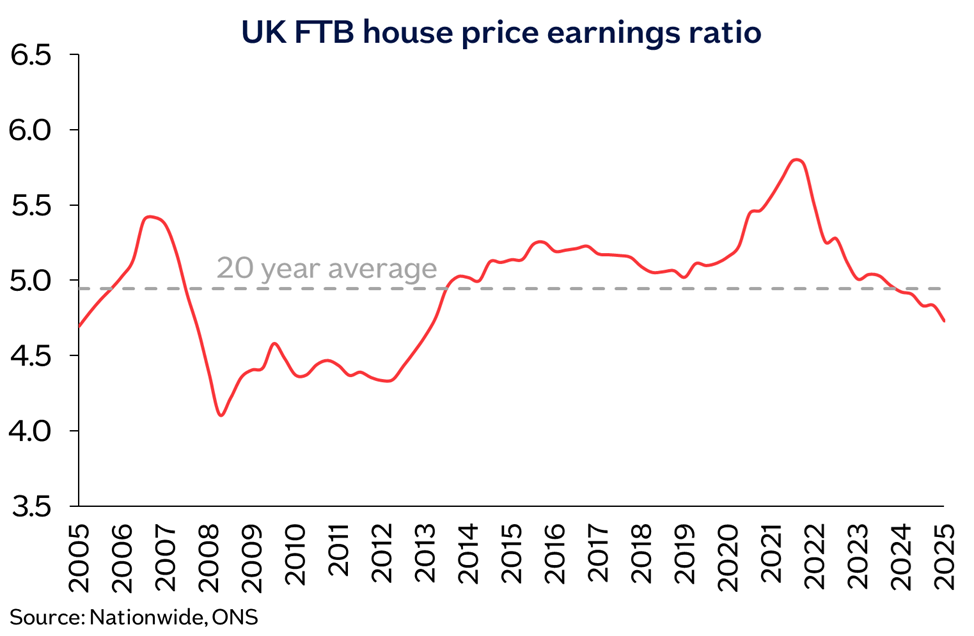

Nationwide’s analysis shows that affordability has actually been improving, driven by two key factors earnings growth outpacing house price growth and falling mortgage rates.

The house price to earnings ratio for first-time buyers has fallen to 4.7 slightly below its 20 year average. Monthly mortgage payments now represent 32% of take-home pay for a buyer purchasing a typical first-time buyer property with a 20% deposit. That’s above the long-run average of 30% but far below the 48% peak.

This improvement has translated into tangible market activity. First-time buyer transactions in 2025 were approximately 20% higher than in 2024. The proportion of high loan to value lending (deposits of 15% or less) reached its highest level in over a decade.

Yet despite this progress, the perception gap still exists. As the BSA research shows, 59% of aspiring buyers have less than £10,000 in savings and believe it will take an average of 6.5 years until they can buy a home. The reality is that many could act far sooner with the right information and products.

THE GEOGRAPHY OF OWNERSHIP

The housing affordability crisis is not one crisis but many, varying by region and deeply intertwined with local economic structures and income levels.

London exemplifies the extremes. A 10% deposit in the capital is over three times larger than the equivalent in the North. Based on saving 10% of average net pay, it would take a Londoner nine years to accumulate their deposit, versus around four years for someone in the North. The capital’s house price to earnings ratio stands at 7.5, more than twice Scotland’s 2.9.

In London, the average earnings of actual first-time buyers are approximately 45% higher than average regional incomes. This suggests that only higher earners are clearing the affordability bar in the capital, while many on average or below average incomes are effectively locked out.

In Scotland and the Midlands, by contrast, actual first time buyer earnings sit much closer to, or even below, regional averages. Mortgage payments as a share of take-home pay in the North, Yorkshire and The Humber and Scotland are actually below their long-run averages. In these regions, homeownership remains relatively accessible to people on typical incomes (although specific markets, such as Edinburgh, still have affordability challenges).

THE OCCUPATIONAL DIVIDE

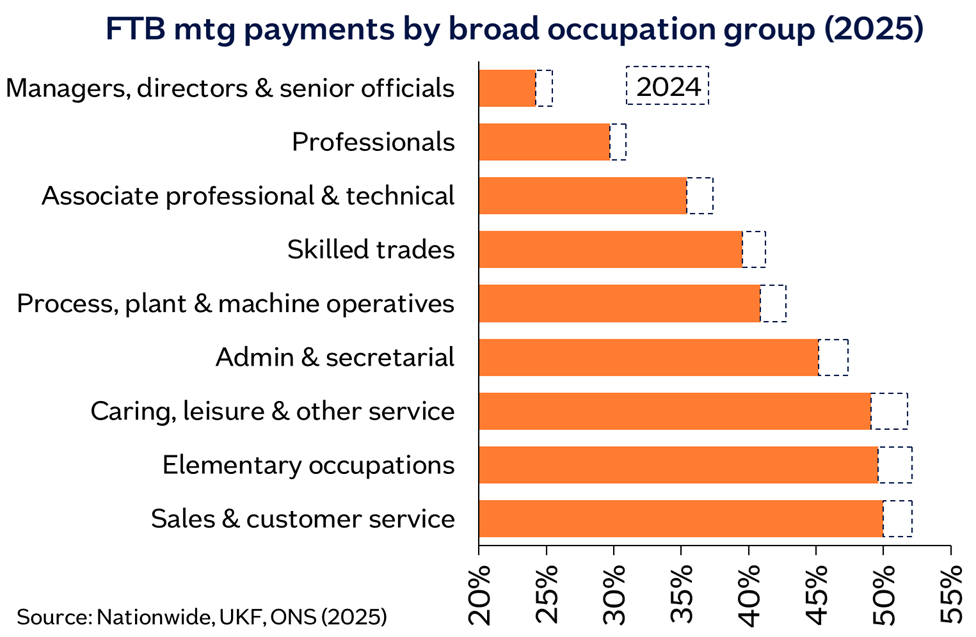

If geography determines who can buy, occupation increasingly determines where that becomes possible. Nationwide’s occupational analysis reveals stark disparities in housing affordability across professional groups.

Managers, directors, and senior officials unsurprisingly face the most favourable conditions, with typical mortgage payments representing about 25% of take home pay. Professional occupations follow close behind at around 27%.

For those in sales and customer service roles, and particularly for workers in “elementary occupations” (construction laborers, cleaners, couriers), mortgage payments would consume approximately half of take home pay.

Caring, leisure, and service occupations saw the largest improvement in affordability during 2025, benefiting from above-average wage growth. All occupational groups experienced some improvement year on year. This is a positive trend, but one that still leaves significant cohorts effectively priced out of homeownership.

This occupational difference has implications for regional housing markets. In high cost areas like London and the South East, only those in higher paid professional and managerial roles can realistically afford to buy. In the North and Scotland, the occupational profile of potential first time buyers is far more diverse, encompassing a broader slice of the income distribution.

THE BANK OF MUM AND DAD AND THE WEALTH DIVIDE

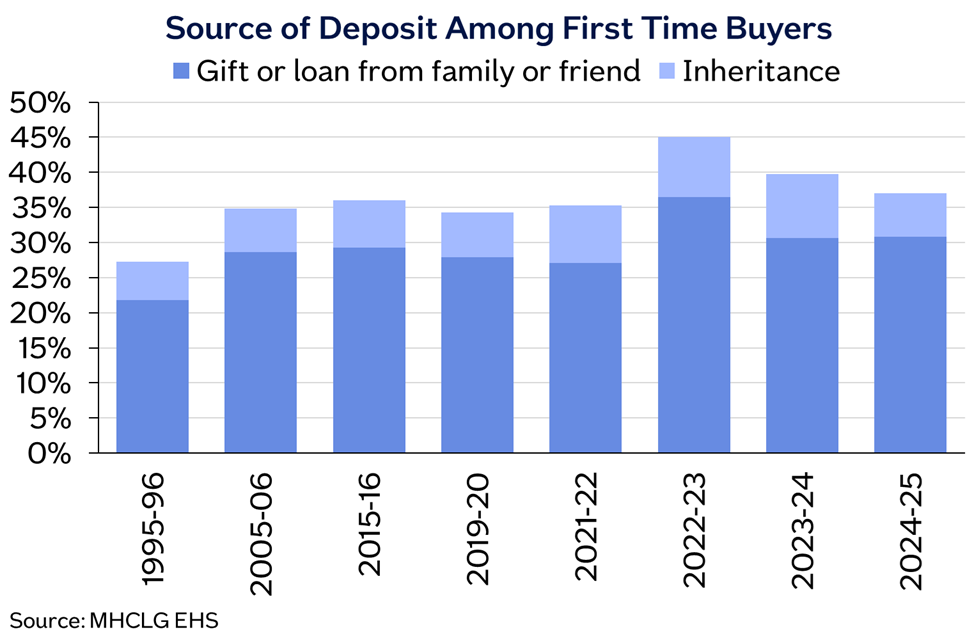

Behind the improving statistics lies an uncomfortable truth about intergenerational wealth transfer. In 2024/25, over one third of first time buyers received assistance in raising their deposit as either a gift or loan from family or friends, or through inheritance.

The “Bank of Mum and Dad” phenomenon has become a structural feature of the UK housing market. Those with access to family wealth can enter the market at younger ages and/or in more expensive areas.

Those without these resources face significantly longer savings times, delayed homeownership, and potentially permanent exclusion from higher cost regions. This has knock on effects in terms of relationships, starting a family and taking up jobs or other opportunities

The BSA research found that 20% of aspiring buyers are holding back on committing to their partner or getting married until they become homeowners. More than a quarter (27%) are postponing starting a family. Around 18% are delaying starting a business. Housing unaffordability isn’t just preventing people from buying property, it’s reshaping the entire timeline of adult life and slowing down the economy.

THE TRUST DEFICIT AND INFORMATION FAILURE

The perception gap identified in the BSA research points to a fundamental information failure in the housing market. When asked what would help them most, 48% of aspiring buyers said they need better understanding of available products, while 44% want clearer information about deposit requirements.

The good news is that trust in professional advice remains strong. Mortgage advisers are viewed as the most reliable source of information (53%), followed by financial services providers (43%). This suggests that directing people toward professional guidance could have significant impact.

However nearly half have never taken that step and the research suggests a combination of factors. These include the perceived complexity of mortgage products, assumption that they don’t qualify and the psychological protection of not confronting disappointment.

Paul Broadhead, Head of Mortgages and Housing Policy at the BSA, captured this dynamic well: “Too many aspiring first-time buyers assume homeownership is off the table without ever checking what is actually available to them.” When the barrier is partly perceptual, the solution must address both the financial reality and the psychology of exclusion.

MARKET TRENDS AND POLICY IMPLICATIONS

Both the BSA and Nationwide expect modest improvements to continue. Nationwide’s Andrew Harvey notes that “housing market activity should strengthen a little further as affordability continues to improve gradually via income growth outpacing house price growth and a further modest decline in interest rates.”

This optimistic outlook is grounded in trends including continued wage growth, particularly in lower paid sectors, mortgage rates at more sustainable levels and the demonstrated willingness of building societies to serve higher loan to value borrowers.

However, several risks loom. Inflation remains a concern and any resurgence could prompt interest rate increases that would quickly erode recent affordability gains. Economic uncertainty, both domestically and globally, could also dampen wage growth or increase unemployment. Finally, any sustained increase in house prices that outpaces earnings growth would reverse the recent positive trend.

POLICY PATHWAYS: BEYOND THE 1.5 MILLION HOMES TARGET

The Government’s commitment to building 1.5 million new homes represents essential long-term supply-side intervention. As Baroness Taylor, Lords Minister for Housing, acknowledged in the BSA press release, boosting supply is fundamental to creating more opportunities for first-time buyers. Government needs to continue with planning reforms and other support to build more houses.

We know new supply won’t solve the immediate challenges facing prospective buyers. Three key policy interventions could complement housing construction:

- Further regulatory change to support mortgage lending. Changes put in place around mortgage stress rates and the loan to income cap have already helped more first time buyers access a home. As well as ensuring potential buyers know about these changes a further reform to enable more access to part interest only part repayment mortgages for first time buyers would help some people access lower additional monthly payments. The FCA is looking at this and progress is expected during 2026.

- Support with deposit saving. The complexity of the Lifetime ISA, its relatively low house price cap in some parts of the country and withdrawal penalties have meant it does not have the impact it could. Government is expected to consult on a simpler Government backed saving product which will be closer in design to the old Help to Buy ISA and should provide more effective support. A higher price cap will be essential if this new scheme is to have it’s maximum impact.

- Sensible introduction of private rented sector reform. Many potential first time buyers will be living in the PRS and facing the challenge of saving for a mortgage deposit while also paying rent. Government activity in the sector including the Renter’s Rights Act and tax changes come with an implied sense they are aiming to favour buyers over landlords. However, too much pressure on landlords can cause them to leave the market and for rents to increase. Listening to landlord concerns and carrying out reform in a sensible well managed way will be better for everyone.

HAVE THE CONVERSATION

All of these policy interventions will take time to design and implement. The BSA has made clear there’s one action that could help thousands of people straight away – speaking to a mortgage lender or broker.

As Economic Secretary to the Treasury Lucy Rigby noted: “Too many people are giving up on owning a home before they’ve even spoken to a lender.”

The 67% of aspiring buyers who said they could purchase sooner than they thought, after seeing what products actually exist, represents a significant group who could take action now with the right information.

Consistent action is needed from Government, regulators and mortgage lenders to keep taking action to support first time buyers. From helping people to save for a deposit through to making the right mortgage products available, this is starting to happen.

The combination of better policy, market innovation and individual action could turn the perception of impossibility into the reality of home ownership for many more families.

The question is whether we’ll close the gap between perception and reality before people give up on the home ownership dream altogether.