It appears as though the housing market resumed normal service in February, writes Jason Tebb. A ‘normal market’ is not to be sniffed at after two years of high levels of uncertainty around the macro-economic picture, governmental shifts, policy changes and the mini-Budget chaos which caused so much upheaval and soaring mortgage rates. Thankfully, the situation has calmed with our data suggesting we are back to more conventional seasonal markets with good levels of confidence prevailing across the board.

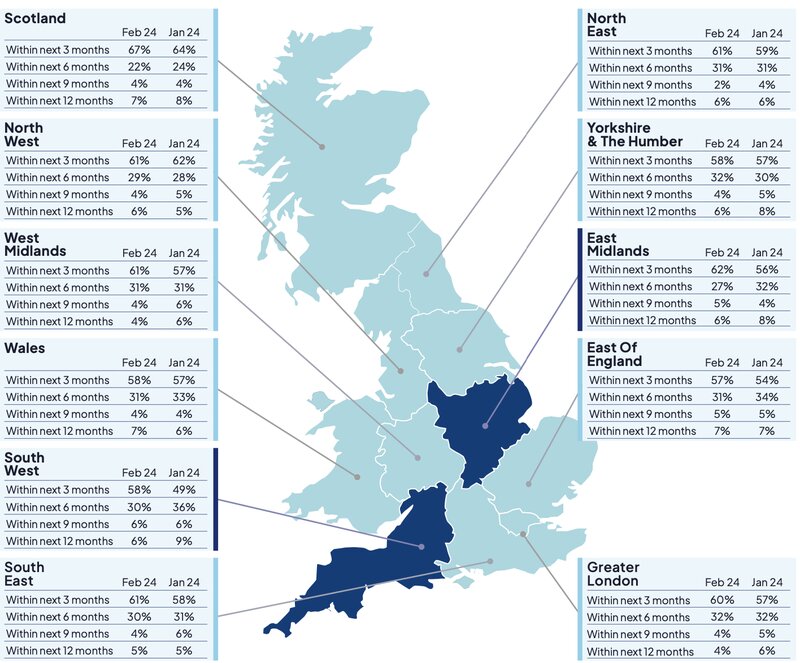

Buyer confidence continues to be stable – in February, 65% of UK buyers were confident they’d purchase a property within the next three months, unchanged from January. Meanwhile, seller confidence improved, with 60% of vendors confident they’d sell within three months, an improvement on January’s 57%. This may reflect the growing conviction around the likely trajectory of interest rates, with another rate hold in February further confirming expectations that rates have peaked and the next move will be downwards.

BUSINESS OF MOVING

Sentiment suggests buyers and sellers are simply getting on with the business of moving. While inflation may still be twice the Bank of England’s 2% target, the worst of it seems to be behind us. Stock levels have increased, as one would expect at this time of year as normal seasonal aspects play out. While property prices have come off their peak a little in the past year, indices report a gentle uptick in national average prices rather than a continuing decline in values. As our data shows, there are regional variations with micro-markets behaving differently depending on local demand and stock levels. Overall though, the outlook for the market this year is far more positive than was the case several months ago.

SECURING A MORTGAGE

Borrowers grew more concerned about securing a mortgage in February, with 8% either very or slightly concerned compared with 6% the previous month. This reflects rising mortgage rates, with lenders increasing their ‘best buy’ deals in February on the back of higher Swap rates, which underpin the pricing of fixed-rate mortgages. January’s mortgage rate war appears to have been shortlived yet borrowers seem to be coming to terms with the new normal – higher rates of around 4 or 4.5% rather than sub-1%, which simply wasn’t healthy or sustainable. There is bound to be a period of adjustment as borrowers are weaned off cheap credit, which will cause concerns around affordability, but those who want to move will have to adapt.

NERVOUSNESS

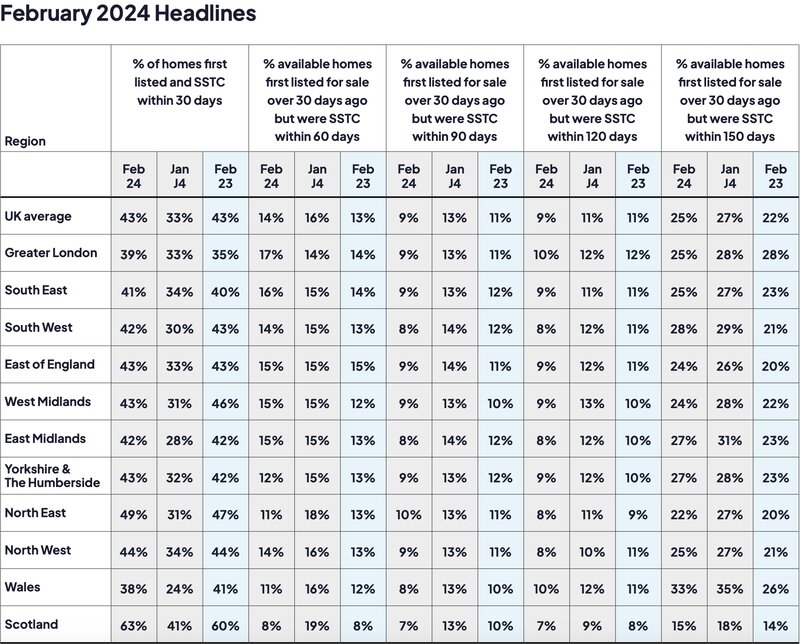

The data suggests they are doing so, with the worst of the nervousness about the market behind us as levels of properties Sold Subject to Contract within 30 days of first being listed increased to 43% in February, from 33% in January. As we move into spring, traditionally a busy time for the housing market when the leaves are budding on the trees and gardens look so much more inviting, transactions are picking up, with encouraging mortgage approval figures from the Bank of England. Buyers and sellers have been sitting back and waiting for some degree of stabilisation, which is where we find ourselves, notwithstanding the general election on the horizon. While there may still be bumps in the road, it feels as though the housing market is morphing into a more sustainable, encouraging state than the boom and bust of the past.