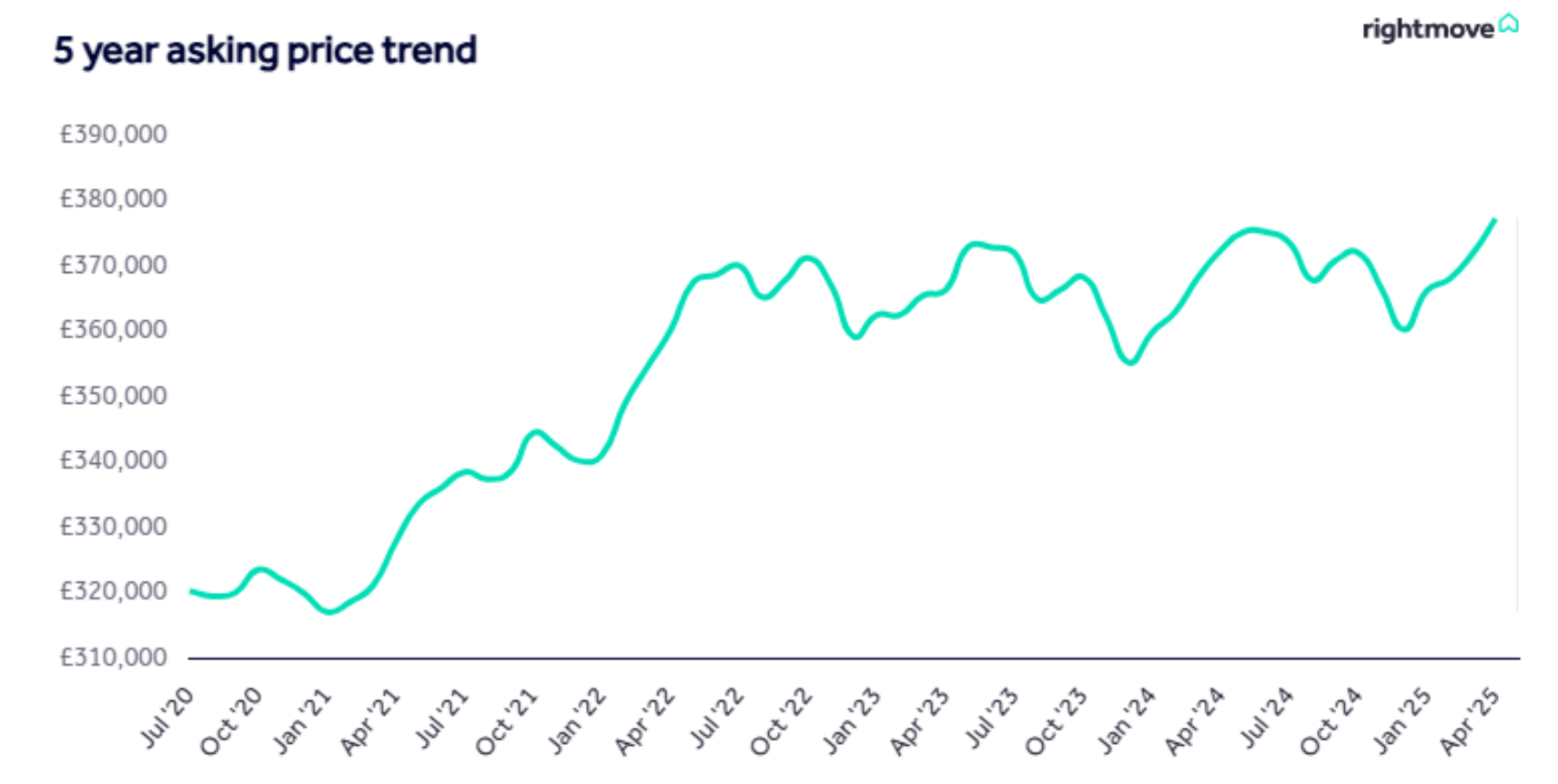

The average price of property coming to the market for sale rose by 1.4% (+£5,312) this month to a new record of £377,182, latest research from Rightmove reveals.

This is the first monthly price record since May 2024, with asking prices and activity typically higher during the Spring season.

In a sign of continuing market resilience, this month’s price increase is larger than the average April increase of 1.2%, despite the number of available homes for sale remaining at a 10-year high for the time of year.

Whilst a seasonal increase in asking prices is a positive sign for the health of the market, new sellers need to be cautious of the high competition for buyers that they may face when setting their asking price.

REALISTIC PRICING

Rightmove’s research shows that homes that are priced realistically from the start of marketing, rather than reduced later, are more likely to find a buyer, and in less than half the time on average.

Meanwhile, the latest snapshot of market activity suggests that the stamp duty increase in England on 1st April hasn’t deterred most movers going through the sales completion process, and that new buyers and sellers still feel confident to enter the market.

Over the last few days, the effects of President Trump’s tariff announcements have been unfolding.

TOO SOON TO CALL

And Rightmove says that it’s too early to tell what the repercussions may be on the UK property market but one potential impact of the announcements is that mortgage rates could drop more quickly, boosting buyer affordability.

Colleen Babcock, Property Expert at Rightmove, says: “We’ve seen our first price record in nearly a year, despite the number of homes for sale being at a decade-high.

“The increased choice seems to be bringing more movers into the market, with both buyer and seller numbers up as the market remains resilient.

“Confidence from new sellers is a good sign for the overall health of the market, but they do need to be careful when setting their asking price.

“The high level of supply in the market right now means that buyers are likely to have plenty of homes in their area to choose from, and an overpriced home will stick out for the wrong reasons.

“Our research also shows that getting the price right the first time is key. Homes that don’t need a reduction in price are more likely to find a buyer, and to find that buyer in less than half the time.”

STAMP DUTY IMPACT

Since the stamp duty increase, the level of agreed sales falling through has remained steady.

This indicates that there has been no major pull-out from agreed deals by first-time buyers and home-movers who were unable to complete before the tax rise.

The last-minute rush to complete sales from those who were fortunate enough to be able to beat the deadline, means that the queue of buyers waiting to complete their purchase has eased by nearly 24,000 or 4%.

It’s the first time that this queue has dropped during the month of March since the pandemic in 2020, though it has now started to tick up again.

NEW BUYER DEMAND

Overall, across the full month of March, new buyer demand was 5% higher than at the same time last year, and the number of new sellers coming to market was 4% higher.

Some segments and sectors of the market are faring better than others.

However these are overall averages, and some segments and sectors of the market are faring better than others. In particular, there is a North and South divide in both price and buyer demand trends.

The majority of Midlands and Northern regions, as well as Wales and Scotland, are seeing above average increases in demand versus last year, and all have seen new price records this month.

By contrast, the higher-priced South West and South East are seeing smaller increases in buyer demand and prices.

London appears to be an outlier; despite being the only region with fewer buyers enquiring than at this time a year ago, average asking prices in London have also reached a new record this month, driven by inner London.

With London typically being more exposed to the impacts of geopolitical tensions, as well as currently seeing weaker demand trends, we may see this price trend fall back.

TRUMP’S TARIFFS

The full impacts of President Trump’s tariffs will play out over the coming weeks and months.

If the Bank of England opts for further and faster rate cuts this could lead to mortgage rates reducing.

As it stands, if the Bank of England opts for further and faster rate cuts, starting in May, this could lead to mortgage rates reducing more quickly than anticipated.

Average mortgage rates remain high, and the current average five-year fixed mortgage rate of 4.72% is only slightly lower than the average of this time last year, which was 4.84%.

UNCERTAIN FUTURE

Babcock adds: “It’s important to remember that among records and national trends, Great Britain’s housing market is made up of thousands of diverse local markets, each uniquely responding to market changes and world events.

“London is likely to see greater knock-on effects from US tariffs.”

“London, for example, is likely to see greater knock-on effects from US tariffs than the rest of Great Britain, while Northern regions appear to be performing more strongly post-stamp duty rise. It’s difficult to predict what the next few months will bring, but if mortgage rates reduce more quickly, it would be a helpful boost to buyer affordability.”

ECONOMIC HEADWINDS

Phill Sandbach, Director at John German in the Midlands, says: “March was a very busy month, with more completions than in the post pandemic stamp duty holiday. Solicitors worked really hard to get so many movers through.

“April has started off as a busy month for us, with market appraisal requests, viewings and offers across all of our East and West Midlands offices. We haven’t seen a downturn in our activity yet due to the tariff situation, but we do expect some economic headwinds as a result.

“Indications are that with an expected reduction in mortgage rates over the summer we will see a stable market in the first half of the year. It remains a constant that correct pricing is absolutely key to a successful sale, anything overpriced will be overlooked by buyers.”

HOLDING BACK

Alex Caddy, Manager at Clarkes Estate and Letting Agency in Dorset, adds: “We’ve seen confidence pick up in the market after a bit of a rocky March for us.

“It appears that some would-be-movers may have been holding back to see if last month’s Bank Rate decision and spring statement brought any good news for the housing market, but since then we have seen buyer activity and new listings pick up for the spring season.

“The market is certainly still price sensitive while supply remains high. Things are moving well when priced appropriately, and particularly popular homes can even go for above asking price.

“Naturally, those who may not be in a rush are testing the market with higher asking prices, in those cases viewing requests are far lower, indicating buyers are still price sensitive.”

TARIFF TURBULENCE

Tom Bill, Head of UK Residential Research at Knight Frank, says: “The recent tariff turbulence underlines why sellers need to be realistic when setting asking prices, particularly in a market where supply is rising more quickly than demand.

“The economic backdrop is bumpy but downwards pressure on mortgage rates as financial markets increasingly price in the risk of an economic slowdown will be positive for demand.

“The risk is that tariffs prove to be inflationary and start putting upwards pressure on borrowing costs but we still expect modest single-digit house price growth this year as needs-based buyers drive demand.”

ATTACK BEST FORM OF DEFENCE

Jeremy Leaf, north London estate agent and a former RICS Residential Chairman, says: “Attack is the best form of defence for some sellers.

“In our offices we have also noticed many want to tough out the loss of the stamp duty concession last month, keep asking prices up and letting the market find a new ‘normal’.

“Others are recognising that the inevitable drop in demand must be reflected in a modest fall in prices at least in order to generate viewings and offers. That is to say nothing of the impact on confidence due to domestic and international economic uncertainty.

“Fortunately, most are sitting on their hands hoping this will pass, which is helping keep fall-through rates and renegotiations to a minimum.”

STRONG MOMENTUM

Nathan Emerson, Chief Executive of Propertymark, says: “It is encouraging to witness the housing market continue to deliver growth, despite the increasingly complex economic challenges we face at the moment.

“Although the rush from many people in England and Northern Ireland to beat stamp duty threshold changes has now concluded, we now progress into the spring and summer months, which typically deliver strong momentum for the sector.

“We remain in a position where inflation is on a potential uneven footing, and this may impact any decision the Bank of England might make regarding interest rates when they next meet on 8 May.”

RATE CUTS

And Tomer Aboody, director of property lender MT Finance, adds: “So far this year it has been a positive few months for the housing market with transaction levels improving, although still below pre-pandemic levels.

“This comparatively subdued activity illustrates how big an impact higher interest rates have had on the market and sentiment.

“All eyes are on the Bank of England to see whether there will be a further reduction in May, with any assistance here likely to boost activity now that the stamp duty concession has ended. Indeed, buyers may await further reductions before making their move.”