Mortgage lending rose sharply in September as homebuyers took advantage of easing borrowing costs and greater market confidence ahead of the Autumn Budget, according to the latest Money and Credit data from the Bank of England.

Net borrowing of mortgage debt by individuals climbed to £5.5 billion, up from £4.3 billion in August and marking the highest level since March 2025.

The annual growth rate for mortgage lending rose to 3.2%, its strongest pace since January 2023.

Gross mortgage lending totalled £24.9 billion in September, compared to £23 billion the previous month, while repayments also edged higher to £20.3 billion.

APPROVALS INCREASE

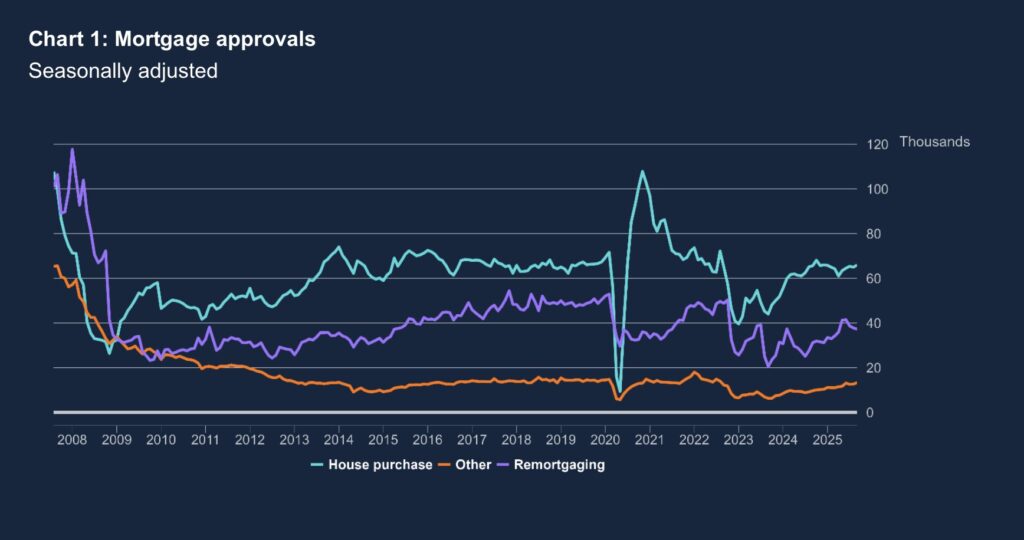

Mortgage approvals for house purchase – a leading indicator of future activity – increased slightly to 65,900, their highest in five months.

However, approvals for remortgaging dipped by 600 to 37,200, suggesting many borrowers are opting to stay with their existing lenders as competition among banks and building societies intensifies.

The average rate paid on newly drawn mortgages fell for a sixth consecutive month, dropping by 7 basis points to 4.19%, the lowest level since January 2023. The rate on the stock of outstanding mortgages was unchanged at 3.89%.

Economists said the figures pointed to a modest revival in the housing market as expectations of rate cuts in 2026 continue to build.

Elsewhere, consumer credit growth softened slightly, with net borrowing falling to £1.5 billion from £1.7 billion in August.

Within that, credit card borrowing was steady at £0.7 billion, while other personal loans and car finance fell to £0.8 billion.

Despite the monthly dip, annual growth in consumer credit ticked up to 7.3%, with credit card borrowing rising 10.8% year-on-year.

Meanwhile, households continued to build savings, depositing £7.9 billion with banks and building societies in September – largely into easy-access and ISA accounts.

The figures suggest that, while consumers remain cautious, falling mortgage rates and a more stable economic outlook could support a gradual recovery in housing market activity through the final quarter of the year.

INDUSTRY REACTION

Richard Donnell, Executive Director at Zoopla, says: “Demand for mortgages to buy homes continues to increase but at a slowing rate as the rolling total over the last 12 months starts to level off as housing transactions reach close to their 10 year average of 1.2m.

“While Budget speculation has hit demand and sales for homes over £500,000, the rest of the market is less affected which explains the continued demand for mortgages.”

APPETITE AND DEMAND

John Phillips, CEO of Spicerhaart and Just Mortgages and says: “While there has been plenty of talk of a holding pattern pre-Budget, today’s figures show that this isn’t the case for all borrowers.

“An increase in approvals in September demonstrates the appetite and demand that still exists in the market – whether that’s those pushing ahead with plans, or perhaps more likely, those that need to move rather than necessarily wanting to right now.

“Either way, the figures reflect what we are seeing across our estate agency branches and our brokerage with relatively robust figures for new buyer registrations, valuation requests and mortgage appointments.

“We are seeing an element of wait and see right now.”

“There’s no doubt we are seeing an element of wait and see right now, which hopefully gives way to some pent-up demand once the Budget is cleared and everyone knows the lay of the land. With these figures in mind though, the message to brokers is to remain on the front foot and be there to support those that are navigating the market. Just as important is the role we play in nurturing confidence among clients, highlighting the many opportunities available and encouraging them to push on with their plans.”

TOUGH RENEGOTIATING

Jeremy Leaf, north London estate agent and a former RICS Residential Chairman, says: “Mortgage approvals always provide the best evidence of likely market activity over the next quarter at least.

“These figures show that prospective purchasers are setting aside concerns about new taxes in the Budget, for the time being at least.

“On the ground, we are seeing plenty of resilience and a grim determination to keep transactions running even though they are becoming more protracted and often subject to some tough renegotiating.”

BUYER RESILIENCE

Jason Tebb, President of OnTheMarket, says: “While speculation surrounding the Budget may have dampened an autumn bounce in the housing market, approvals for house purchases – an indicator of future borrowing – increased in September regardless, demonstrating resilience and determination from buyers and sellers to get on with their moving plans.

“With the rate on newly-drawn mortgages falling again for the seventh consecutive month, affordability challenges continue to ease. Although the Bank of England held rates in September, this stability, following five base rate cuts over the previous year, has helped confidence.

“As swap rates continue to fall, and with lenders keen to do more business before the end of the year, some are lowering their mortgage rates, which is further good news for borrowers.”

STRONGER POSITION

Nathan Emerson, Chief Executive of Propertymark, says: “An uplift in the number of mortgage approvals is encouraging to witness.

“Many cogs need to turn harmoniously together when it comes to consumer confidence and affordability, and despite challenges within the wider economy, it is positive to see people being able to take their next step onto the housing ladder with greater ease.

“There are still concerns which need to be acknowledged, however, such as inflation sitting close to double what the Bank of England have targeted and the influence this can have regarding base rate decisions.

“Despite this, we remain in a much stronger position than we started the year at, when the base rate stood much higher at 4.75%.”

STILL STRONG DEMAND

Mark Tosetti, Chief Executive of CAL (part of Movera), says: “An uptick in net borrowing and slight increase in net mortgage approvals indicates that there is still strong demand in the market and that we have emerged, tentatively from a slow summer.

“But the looming Autumn Budget is clearly continuing to put a damper on consumer confidence, with the latest data from Zoopla – released earlier this week – suggesting buyer demand is down 8% compared with last year and sales agreed have fallen by 3%.

“However, as inflation fell short of the Bank of England’s 4% forecast this month, the MPC’s base rate decision next week could provide a lifeline for the sector and generate some more attractive interest rates from lenders.”

STICKY INFLATION

Joe Pepper, UK Chief Executive Officer, PEXA, says: “Sticky inflation and interest rates remaining has created a little bit of apathy in the market – people are no longer waiting for a better rate environment to buy or remortgage because they aren’t necessarily expecting this to happen any time soon.

“Empowering more individuals to confidently mortgage and remortgage. We are also starting to see the positive impact of affordability measures introduced earlier this year and it is positive to see the market start moving in the right direction.

“However, as mortgage approvals increase, bottlenecks form across the market because the technology that sits behind the transaction process simply isn’t up to the job.

“Conveyancers, who are already under significant strain, will be pushed to their limits because they don’t have the right tools and technology in place to help them deal with demand.

“We need far greater attention placed on reforming the back-end infrastructure that supports the process to overcome this, delivering a more certain, secure and streamlined process. Addressing this could not be more urgent if we are going to maintain growth and reap the benefits.”

SHIFTING MOOD

Ian Futcher, Financial Planner at Quilter, says: “While the data paints a positive picture of September, the mood in the market has since shifted. With the Budget now fast approaching and rumours brewing about potential changes to housing taxes or stamp duty reliefs, many people are growing more cautious.

“Decisions about buying or selling a home are increasingly being put on hold until there is greater clarity on what the Chancellor will do. A small recent rise in mortgage rates has only reinforced that sense of hesitation.

“These figures capture the last of the late-summer confidence before pre-Budget uncertainty set in. Many people are now pressing pause on big decisions until they know whether upcoming policy changes will alter the costs of owning property or moving home.

“For households trying to plan, staying informed and waiting for full details before making major financial moves could prove wise in the weeks ahead.