House prices and sales volumes are expected to grow in 2025 despite budget headwinds, the latest House Price Index from Zoopla reveals.

The average house price is currently £267,200 having increased by 1.5% over the last 12 months (an increase of £3,900).

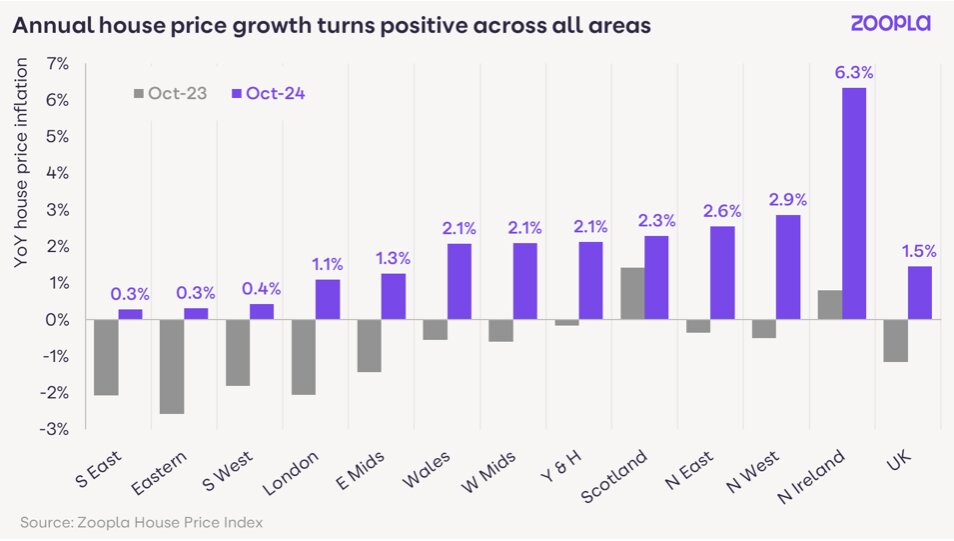

The housing market returned to growth in 2024, with UK house prices recording average growth of +1.5% in the 12 months to October 2024, up from -1.2% a year ago.

All regions and countries across the UK have recorded positive year-on-year growth, with the fastest price gains registered in Northern Ireland (6.3 per cent) and the North West region (2.9 per cent).

AFFORDABILITY PRESSURES

House price growth remains below 1% across southern England where affordability pressures are an ongoing drag on the scale of house price growth.

House price growth remains below 1% across southern England where affordability pressures are an ongoing drag on the scale of house price growth.

Sales agreed over the last four weeks are currently up 19 per cent year-on-year, with buyer demand 25% higher over the same period.

The sales market is on track for 1.1m sales completions over 2024 – 10% higher than in 2023.

And sales completions over 2025 will be supported by a robust sales pipeline, 30% larger than this time last year, which is expected to deliver a strong start in the first few months of next year.

Zoopla expects the number of sales to increase by 5% over 2025 increasing to 1.15 million.

Postponed home moves, an ageing population, rising running costs and changing working patterns will continue to impact moving decisions, in addition to the desire to seek a better home or location.

First-time buyers are also expected to remain the largest buyer group, supporting housing chains and helping existing homeowners to move.

Zoopla says that rising incomes have helped to reset housing affordability over 2024 in the face of higher borrowing costs.

DISPOSABLE INCOMES INCREASING

Data from the Office for Budget Responsibility (OBR) shows household disposable incomes increasing by 15 per cent between 2022 Q2 and 2024 Q22.

House prices grew by just 1.5% over the same period, a trend that has helped to repair housing affordability without the need for additional support from a fall in house prices.

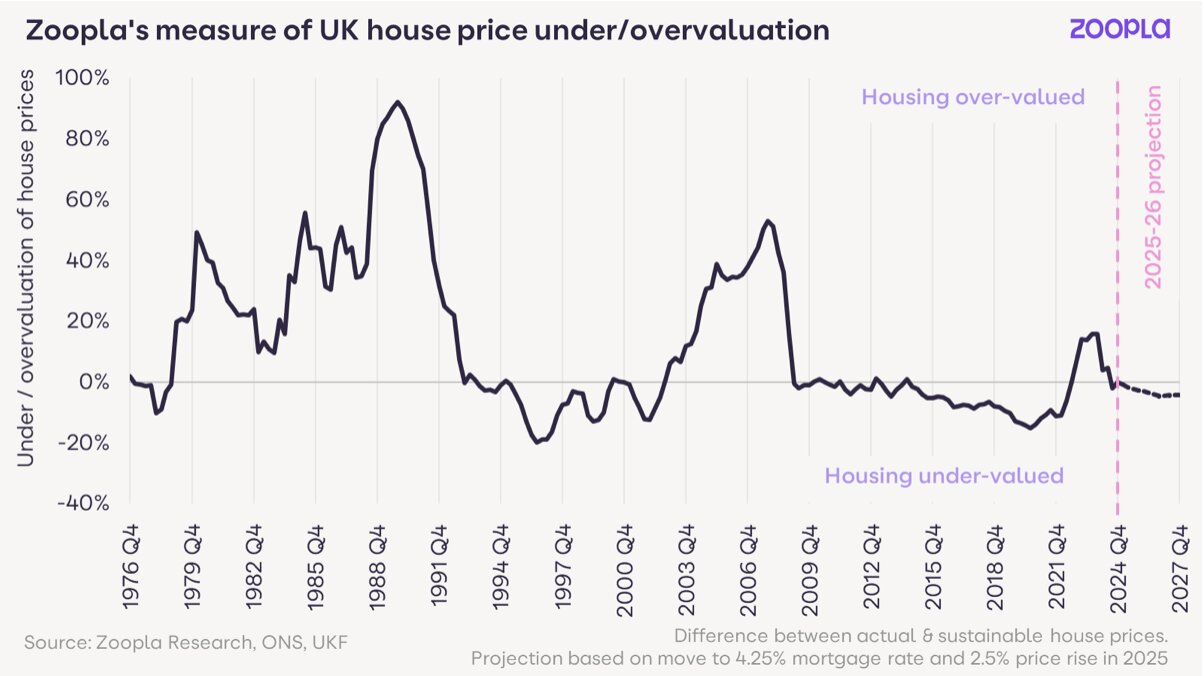

Last year Zoopla reported that UK homes were over-valued by 16% because of the jump in mortgage rates. Rising incomes and lower mortgage rates over 2024 have removed this over-valuation without the need for prices to fall further in 2024.

This means the housing market has largely adjusted to higher mortgage rates, opening up the opportunity for continued modest growth in house prices which are expected to increase by 2.5% over 2025 assuming mortgage rates average 4.25% over the year ahead.

NORTH-SOUTH DIVIDE

The north-south divide in house price inflation will remain over 2025, a continuation of current trends.

Affordability and access to housing is better outside southern England where the income to buy remains high and a drag on house price inflation.

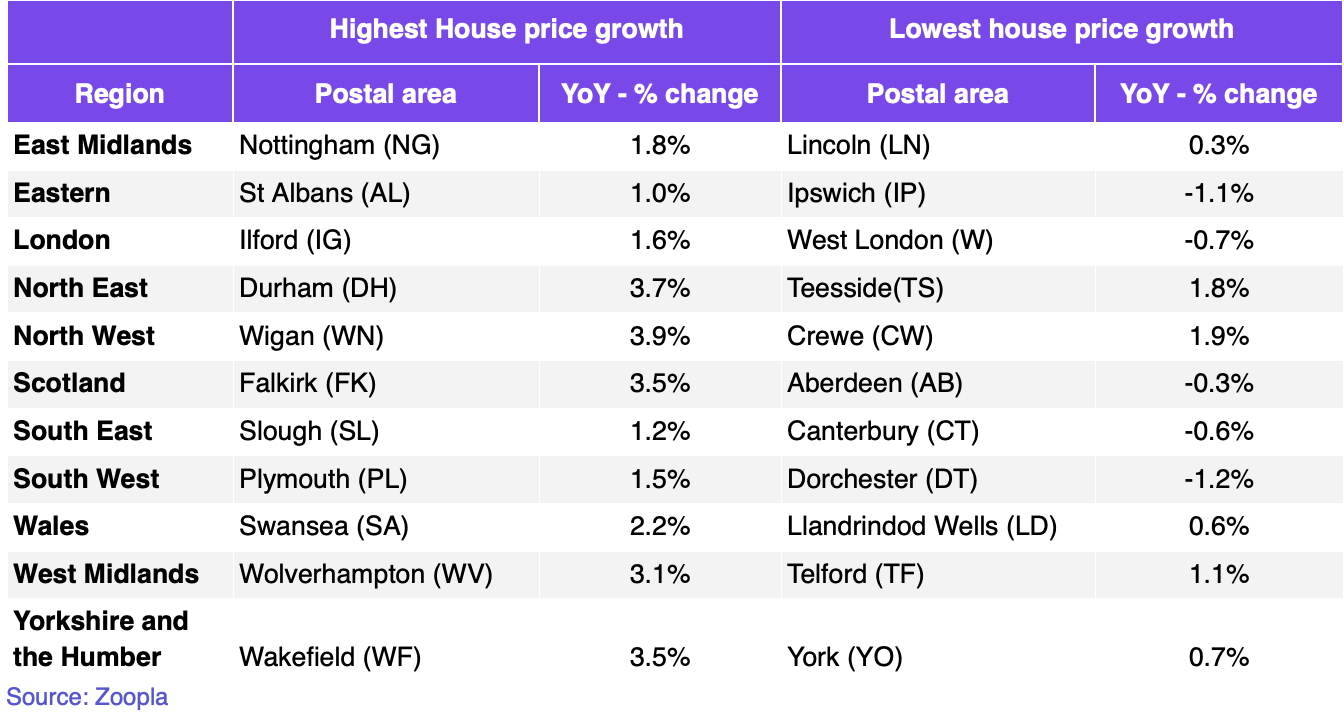

This north-south divide is evident at a local level with the fastest price rises being registered in the Oldham (OL, 3.7%), Wigan (WN, 3.9%) and Belfast (BT, 6.5%) postal areas. In contrast, modest price falls are still being recorded in pockets of southern England led by Ipswich (IP, -1.1%), Truro (TR, -1.2%) and Dartford (DT, -1.2%).

Incomes will need to grow faster than prices to improve affordability, with house prices likely to grow in southern England over 2025 and into 2026.

RESILIENT HOUSING MARKET

Richard Donnell, Executive Director at Zoopla, says: “The housing market has been resilient in the face of higher borrowing costs over the last two years.

“Higher income growth and lower mortgage rates have helped reset housing affordability faster than many expected over 2024. This has supported an increase in the number of sales and house prices over the year which we expect to continue over 2025.

“House price growth in southern England will continue to lag the UK average and incomes will need to rise faster than prices to help reset affordability and price more households into the market.”

And he adds: “First-time buyers will remain an important buyer group but existing homeowners looking to move will need more support to help realise their ambitions, with more and more having to look further afield to find better value for money.”

MORE BUYERS

Matt Thompson, Head of Sales at estate agency Chestertons, says: “As we are approaching the end of the year, we are already seeing more buyers entering the market which is not typical for this time of year and a strong indication that 2025’s property market will be buoyant.

“One reason for the uplift in buyer activity are changes to stamp duty, announced in the Autumn Budget. These will come into effect in April 2025, driving first-time buyers in particular to get on the property ladder before that deadline and will fuel a busy start to next year’s property market.”

BUYER DEMOGRAPHICS

He adds: “Other buyer demographics, including families, couples, professionals and downsizers considered 2024 a challenging year to buy a property amid political and economic uncertainty but now feel more motivated to resume their search in the new year.

“Contributing to the return of buyer confidence are lower interest rates, slightly more attractive mortgage products and the fact that the market has benefited from an uplift in the number of properties being put up for sale.

SUPPLY AND DEMAND IMBALNCE

“Despite house hunters having a slightly larger selection of properties to choose from in 2025, pent-up demand will result in most properties attracting multiple buyers which will make for a competitive property search – especially in London and other sought-after destinations across the UK.

“Due to an ongoing imbalance between supply and demand, most sellers will insist on achieving their asking price. As such, we predict properties in the capital to hold their value or see a gradual increase of up to 3 per cent over the course of next year.”

ECONOMIC PLAN

Tom Bill, head of UK residential research at Knight Frank, says: “After a prolonged wait for the Budget, the biggest remaining uncertainty for the housing market is whether Labour’s economic plan will work.

“If there is extended upwards pressure on unemployment, inflation and borrowing costs, a period of stagflation would put downwards pressure on house prices and transaction volumes.

For now, post-Budget certainty and mortgage rates agreed before 30 October are underpinning momentum.”

IMPROVING AFFORDABILITY

Toby Leek, NAEA Propertymark President, says: “With interest rates easing and affordability improving, many buyers will have increased confidence and may be presented with better mortgage offers compared to what they were seeing at the start of the year in order to make their next home purchase a reality.

“The market is set to see a continued spike in homes for sale and serious buyers coming to the fore despite winter months historically being a quieter time due, in part, to many people across England and Northern Ireland wanting to complete before the rises to stamp duty commence from April 2025.”